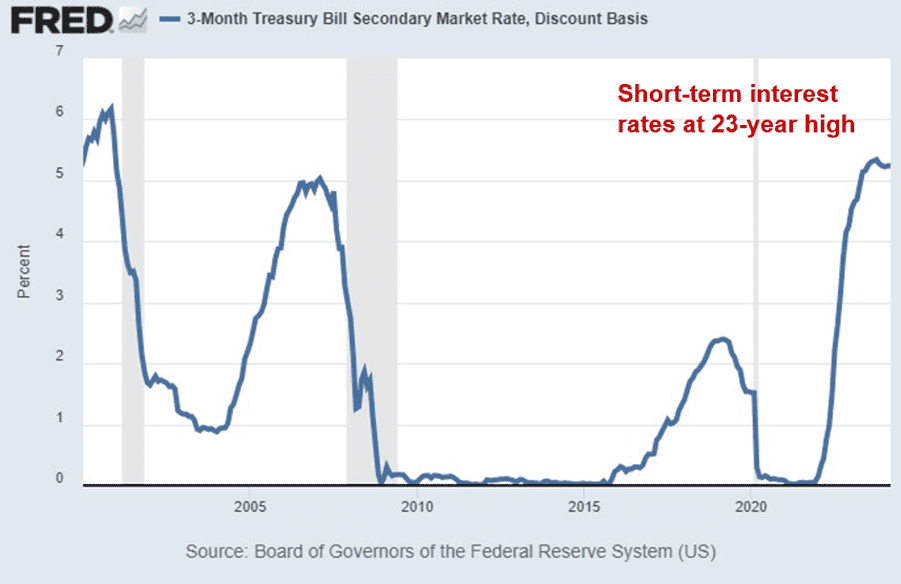

For the first time since the turn of the millennium, investors are being paid to hold cash. Short-term bonds, CDs, money market funds, and high yield savings accounts are sporting interest rates north of 5%, the highest levels seen since 2000. Furthermore, with consumer price pressures moderating, cash and cash-like investments are providing a positive real return of about 2% after inflation while offering a high degree of safety. What’s not to like?

Don’t expect it to last forever. As inflation continues to approach the Federal Reserve’s 2% target, the central bank is seeking the opportunity to begin reducing interest rates, likely in 3 bites of ¼ point each by year end. Whether this year or next, falling interest rates will soon confront conservative investors with an additional downside risk factor they haven’t faced in over 20 years: reinvestment risk.

This term refers to the inevitable scenario that instruments like bonds, CDs, and even shares in money market funds with higher rates of return must eventually be reinvested in a lower yielding replacement during periods of declining interest rates. For example, it is relatively easy today to find certificates of deposit with interest rates of 5% or more maturing in 6 months. Reinvestment risk refers to the chance that rates will be lower, say 4.5%, when the CD comes due and the cash is reinvested. It is often overlooked or unrecognized by investors and is minimal when rates are rising but becomes particularly relevant at cyclical turning points. Such a cyclical pivot is likely nearing, with the Fed poised to begin easing monetary policy later this year.

Reinvestment risk is frequently underappreciated because it does not represent an overt financial loss, but what economists call opportunity cost, an inferior result due to missing out on a better alternative.

Bond investors are well acquainted with something called interest rate risk, especially since 2022. Rising interest rates in the economy cause market prices of bonds and bond funds to fall, a material if theoretically temporary paper loss that shows up on monthly account statements. Bonds took the biggest hit on record during the Fed’s 2022 rate hiking cycle in response to elevated inflation. The broadest index of investment grade bonds lost 13%, causing many bondholders to flee into cash.

Interest rate risk bites when rates are rising. On the other hand, reinvestment risk manifests as rates are declining, and while it does not show up as a direct loss inside a 401(k), it can erode long term returns.

The risk of reinvesting at less favorable rates is especially prevalent when short rates are higher than longer rates. This is referred to as an inverted yield curve, where 10-year bonds pay less than 6-month bonds, and it is not usual. It has often served as a warning of impending recession, although after nearly 2 years, the current inversion is looking like a false alarm. Still, higher short-term rates encouraged investors to crowd into safe and attractive CDs and money markets to await a more normal climate.

The last time rates were this high was in 2000, a period that presents a classic example of reinvestment risk. In the wake of the dot com crash, an inverted yield curve offered investors a higher immediate return for shorter maturities, analogous to if less pronounced than the present environment. On July 1, 2000, the 10-year US Treasury bond had a yield of 5.9%, compared with 6.1% for a much shorter 1-year Treasury. Then as now, the higher rate on the shorter maturity was tempting, but resisting that temptation would ultimately pay big dividends. One year hence, investors in the 1-year issue faced a measly 3.3% rate when they reinvested in a new 2001 bond, and then an even slimmer 1.8% in 2002. At the end of 10 years, the series of 10 1-year reinvestments yielded an annualized 3.0%, roughly half the return for those who bought and held the 10-year bond and captured the original 5.9% per year throughout the ensuing decade.

Total assets in liquid cash investments in short-term bonds, CDs, and money market funds are at record levels as yields have been attractive. But the salad days of high cash rates may be coming to an end. Bankrate reports that CD rates peaked in late December and have begun to come down, with money market funds likely to follow. Cash and CD yields are closely tied to expectations regarding the Fed Funds rate, the policy rate controlled by the Federal Reserve. Markets are already anticipating Fed cuts and are starting to price them into cash rates. If the path ahead is lower, this is the time to adjust portfolios in anticipation.

Investors should consider adding additional duration to their cash and fixed income holdings. That is, holding more bonds or bond funds with somewhat longer maturities and staggering or “laddering” fixed income over the short to intermediate term (out to 10 years or so). CD investors should also consider laddering into longer maturities. As monetary policy normalizes, short-term interest rates are likely to decline faster than longer rates, gradually restoring the normal positive slope of the yield curve, exposing investors to greater reinvestment risk but offering opportunity in longer maturities.

It has been said that cash is king, certainly true of late, but locking in today’s relatively high rates for longer is a move worth considering before the train leaves the station.